₹60,000 monthly take-home in India in 2026 puts you comfortably above the median salaried professional — but not so comfortable that money manages itself. Between rising rent, ₹150/kg tomatoes, EMIs, and the pressure to "look successful", the gap between earning ₹60k and building wealth from ₹60k is where most Indians silently lose 10 years.

This is a no-fluff, number-heavy plan for the ₹60,000 salary bracket: exact budget allocation, tax under the new 2026 regime, SIP math that builds ₹2 crore in 20 years, and the 5 mistakes that keep this salary from ever feeling like enough.

Ideal ₹60,000 Monthly Budget (Snapshot)

| Category | % of Salary | Amount (₹) | Notes |

|---|---|---|---|

| Rent + utilities | 25% | 15,000 | Cap strictly at this |

| Groceries + food | 15% | 9,000 | Home cooking + limited eat-outs |

| Transport + fuel | 8% | 4,800 | Metro/bike; avoid car EMI at this salary |

| Insurance (term + health) | 4% | 2,400 | ₹1 Cr term + ₹5L health |

| SIP (equity) | 25% | 15,000 | Wealth engine — non-negotiable |

| Emergency fund | 5% | 3,000 | Till 6-month buffer built |

| Retirement (NPS/EPF top-up) | 5% | 3,000 | Long-term compounding |

| Lifestyle + entertainment | 10% | 6,000 | Guilt-free spending |

| Miscellaneous | 3% | 1,800 | Gifts, repairs |

Total: ₹60,000. Save-invest ratio: 35%. That's the number that separates wealth builders from paycheck-to-paycheck.

Detailed Breakdown

Take-Home Reality After Tax (New Regime 2026)

₹60,000/month = ₹7,20,000/year CTC-approximate. Under the new tax regime 2026 with ₹75,000 standard deduction:

- Taxable income: ₹6,45,000

- Tax under new regime slabs (0 up to ₹4L, 5% up to ₹8L): ₹12,250

- Rebate under Section 87A (income under ₹7L): Full rebate

- Final tax payable: ₹0

At ₹60,000/month take-home, your tax liability is zero under the 2026 new regime. No need to hunt for 80C deductions. Verify yours → Tax Calculator India.

Age-Wise Allocation Strategy

Age 22–28 (Single, Early Career)

- Rent ₹12,000 (shared)

- SIP ₹20,000 (100% equity, aggressive growth)

- Skill upgrades ₹5,000

- Lifestyle ₹15,000

- Emergency + insurance ₹8,000

Age 28–35 (Married, No Kids)

- Rent ₹18,000

- SIP ₹15,000 (80% equity, 20% debt/gold)

- Household ₹12,000

- Insurance + emergency ₹6,000

- Lifestyle ₹9,000

Age 35–45 (Family, Kids)

- Rent/EMI ₹18,000

- Kids education fund SIP ₹8,000

- Retirement SIP ₹7,000

- Household ₹15,000

- Insurance ₹4,000

- Lifestyle ₹8,000

SIP Math: ₹15,000/Month → ₹2 Crore in 20 Years

At 12% CAGR (India equity long-term average):

| SIP Amount | 10 Years | 20 Years | 25 Years |

|---|---|---|---|

| ₹15,000 | ₹34.8 L | ₹1.50 Cr | ₹2.85 Cr |

| ₹15,000 with 10% annual step-up | ₹43 L | ₹2.24 Cr | ₹4.75 Cr |

| ₹20,000 with 10% step-up | ₹57 L | ₹2.99 Cr | ₹6.32 Cr |

The magic word is step-up. Every year your salary rises, raise SIP by 10%. That single habit turns ₹15k SIP into ₹2.24 Cr instead of ₹1.5 Cr — a ₹74 lakh bonus for zero extra effort.

Plan yours → SIP Calculator India.

Insurance: The 2 Policies You Must Buy

- Term Life Insurance: ₹1 Cr cover — costs ₹700–₹900/month at age 28. Non-negotiable if anyone depends on you.

- Health Insurance: ₹5 L base + ₹15 L super top-up — costs ~₹900/month at age 30. One hospitalisation without it wipes 2 years of SIPs.

Never buy: ULIPs, endowment, money-back, LIC "investment" plans. They return 4–6% — worse than FD.

Emergency Fund Target

Build 6 months of expenses = ₹2.7 lakh in a liquid fund or high-yield savings. Once built, redirect that ₹3,000/month into SIP.

Calculation Method

SIP future value with step-up:

Each year's SIP grows at (1+r)^remaining years; sum all yearly contributions.

Simple version: use the compound interest formula annually.

FV = Σ [Pₙ × (1+r)^(n)] where Pₙ = SIP amount in year n (with 10% annual step-up), r = 12%, n = years remaining.

Tax under New Regime 2026:

| Slab (₹) | Rate |

|---|---|

| 0 – 4,00,000 | 0% |

| 4,00,001 – 8,00,000 | 5% |

| 8,00,001 – 12,00,000 | 10% |

| 12,00,001 – 16,00,000 | 15% |

| Above 20L | 30% |

Rebate under Section 87A: full tax rebate if income ≤ ₹7L.

Common Mistakes Indians Make at ₹60k Salary

- Lifestyle inflation — every raise gets absorbed by a bigger car, bigger flat, subscription creep. Salary doubles, savings stay flat.

- Buying LIC/ULIP thinking it's investing — 4–6% returns lock your money for 15 years.

- Skipping term insurance — ₹900/month feels wasteful until it isn't.

- EMI stacking — bike loan + phone EMI + credit card revolving = ₹20k/month bleed on discretionary junk.

- Investing without goals — random SIPs in 8 funds. Instead pick 2–3 funds tied to specific goals (emergency, retirement, house).

- Chasing hot stocks/crypto with core money — treat as ≤5% satellite allocation.

- Never negotiating salary — job switches deliver 25–40% hikes; loyalty delivers 8%.

Action Plan: Your First 90 Days

Try on FundGenie

FundGenie builds this exact ₹60,000 plan for your age, city, and goals in 90 seconds — including which mutual funds match your risk profile.

- 👉 Calculate your SIP instantly on FundGenie

- 👉 Check your real tax liability

- 👉 Plan your home loan EMI

FAQs

Q1: Is ₹60,000 a good salary in India in 2026? Yes — it puts you in the top 15% of Indian salaried earners. It's comfortable in Tier-2 cities and manageable in Tier-1 with strict rent control (under ₹18,000).

Q2: How much tax on ₹60,000 salary per month in India? Under the new tax regime 2026, zero tax — thanks to ₹75,000 standard deduction plus Section 87A rebate for income under ₹7 lakh.

Q3: How much should I invest from ₹60,000 salary? Minimum 25% (₹15,000) in equity SIP + 5% (₹3,000) in emergency fund + 5% (₹3,000) in retirement (EPF/NPS) = 35% total save-invest ratio.

Q4: Can I become a crorepati with ₹60,000 salary? Yes. ₹15,000 SIP with 10% annual step-up at 12% return = ₹2.24 Cr in 20 years. First crore hits around year 15.

Q5: Should I choose the old or new tax regime on ₹60k salary? New regime. Your tax is zero either way, but the new regime requires no deduction paperwork and no 80C lock-ins.

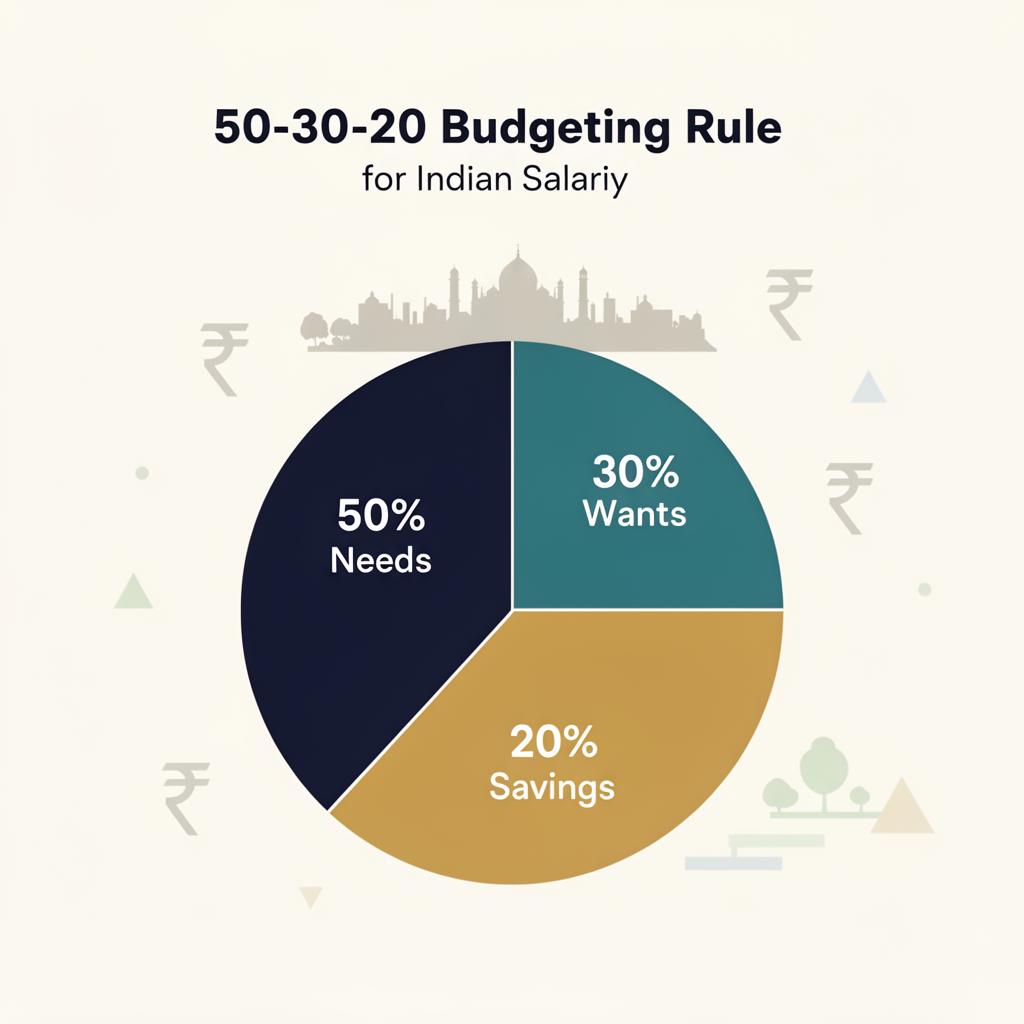

Q6: What is the 50-30-20 rule for ₹60,000 salary? 50% needs (₹30,000), 30% wants (₹18,000), 20% savings (₹12,000). For India 2026 a better version is 50-15-35 — 50% needs, 15% wants, 35% savings and investments — because Indian inflation and future goals demand higher savings.

Q7: How much rent should I pay on ₹60,000 salary? Cap at 25% of take-home = ₹15,000. Any higher and you cannot hit the 35% save-invest ratio.

Q8: Best SIP for ₹15,000 monthly investment? Split as: 60% large-cap index fund (Nifty 50), 25% flexi-cap active fund, 15% mid/small-cap. Increase small-cap only if 10+ year horizon and stable income.

<script type="application/ld+json"> {"@context":"https://schema.org","@type":"Article","headline":"₹60,000 Salary in India: Budget & Investment Plan 2026","author":{"@type":"Organization","name":"Fund Genie"},"publisher":{"@type":"Organization","name":"Fund Genie","logo":{"@type":"ImageObject","url":"https://fundgenie.online/favicon.ico"}},"datePublished":"2026-07-07","mainEntityOfPage":"https://fundgenie.online/blog/60000-salary-india-budget-investment-plan-2026","image":"https://fundgenie.online/blog/60000-salary-india-budget-2026.jpg"} </script> <script type="application/ld+json"> {"@context":"https://schema.org","@type":"BreadcrumbList","itemListElement":[{"@type":"ListItem","position":1,"name":"Home","item":"https://fundgenie.online/"},{"@type":"ListItem","position":2,"name":"Blog","item":"https://fundgenie.online/blog"},{"@type":"ListItem","position":3,"name":"Personal Finance","item":"https://fundgenie.online/topics/personal-finance"},{"@type":"ListItem","position":4,"name":"₹60,000 Salary India Budget 2026","item":"https://fundgenie.online/blog/60000-salary-india-budget-investment-plan-2026"}]} </script> <script type="application/ld+json"> {"@context":"https://schema.org","@type":"FAQPage","mainEntity":[{"@type":"Question","name":"Is ₹60,000 a good salary in India in 2026?","acceptedAnswer":{"@type":"Answer","text":"Yes — top 15% of Indian salaried earners. Comfortable in Tier-2 cities, manageable in Tier-1 with rent under ₹18,000."}},{"@type":"Question","name":"How much tax on ₹60,000 salary per month?","acceptedAnswer":{"@type":"Answer","text":"Zero tax under the new regime 2026 after ₹75,000 standard deduction and Section 87A rebate."}},{"@type":"Question","name":"How much should I invest from ₹60,000 salary?","acceptedAnswer":{"@type":"Answer","text":"Minimum 35% total: ₹15,000 equity SIP, ₹3,000 emergency, ₹3,000 retirement."}},{"@type":"Question","name":"Can I become a crorepati with ₹60,000 salary?","acceptedAnswer":{"@type":"Answer","text":"Yes. ₹15,000 SIP with 10% annual step-up at 12% return reaches ₹2.24 Cr in 20 years."}},{"@type":"Question","name":"Old or new tax regime on ₹60k salary?","acceptedAnswer":{"@type":"Answer","text":"New regime — zero tax either way, with no deduction paperwork."}},{"@type":"Question","name":"What is the 50-30-20 rule for ₹60,000 salary in India?","acceptedAnswer":{"@type":"Answer","text":"Prefer 50-15-35 for India 2026: 50% needs, 15% wants, 35% savings and investments."}},{"@type":"Question","name":"How much rent should I pay on ₹60,000 salary?","acceptedAnswer":{"@type":"Answer","text":"Cap at 25% of take-home = ₹15,000 to preserve the 35% save-invest ratio."}},{"@type":"Question","name":"Best SIP for ₹15,000 monthly investment?","acceptedAnswer":{"@type":"Answer","text":"60% Nifty 50 index fund, 25% flexi-cap active fund, 15% mid/small-cap for 10+ year horizon."}}]} </script>Did you find this useful?