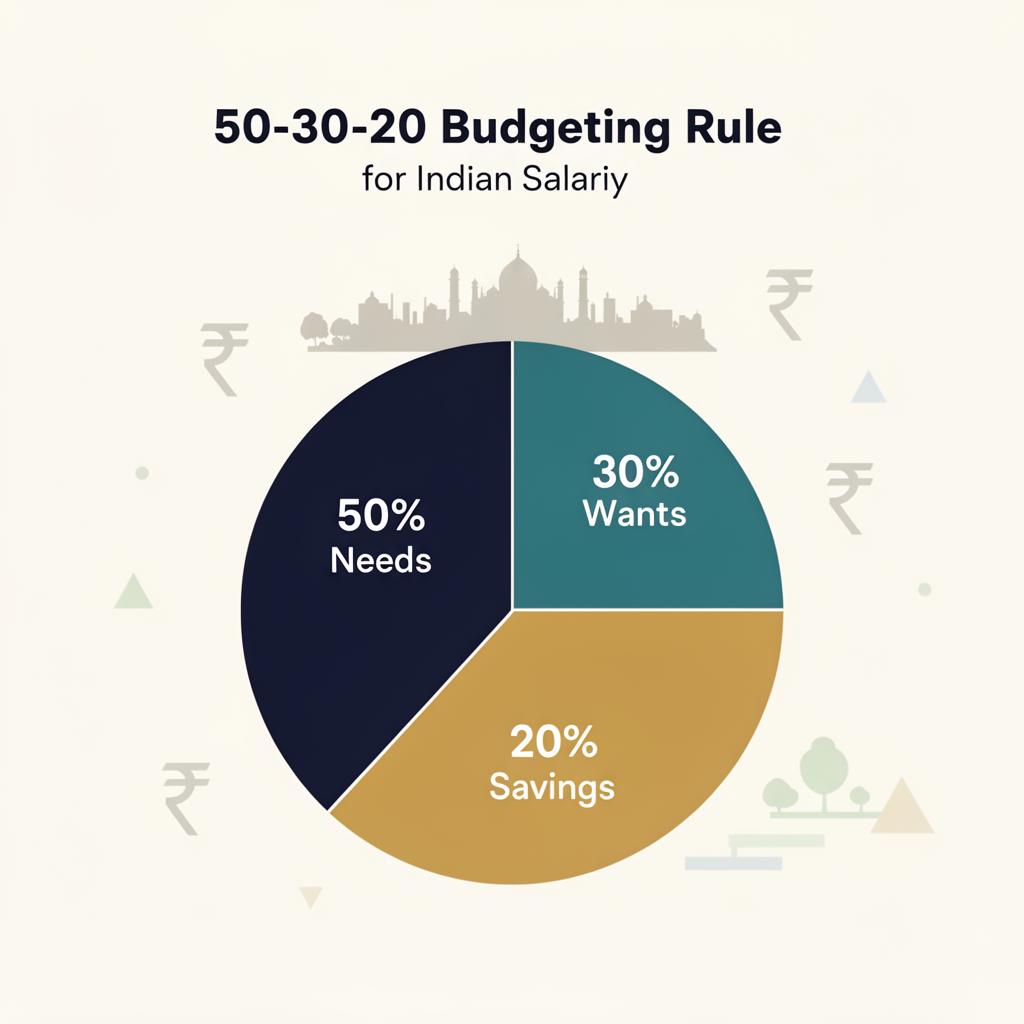

50-30-20 Rule: Does It Actually Work for Indian Salaries in 2026?

Every salaried Indian has heard the 50-30-20 rule at least once — 50% on needs, 30% on wants, 20% on savings. It sounds clean on a US personal-finance podcast. But does it survive a Mumbai 1BHK rent of ₹45,000, a Bengaluru school fee of ₹1.8 lakh, or a ₹22 lakh CTC where in-hand is barely ₹1.4 lakh after PF, tax and HRA games?

With CPI inflation still hovering around 5%, rent compounding 8–10% a year in metros, and EMIs eating 40–55% of take-home in most households, the 50-30-20 rule needs an Indian rewrite — not rejection. This 2026 guide breaks down whether it works, where it breaks, and the realistic version you should actually follow.

Quick Summary: 50-30-20 on Real Indian Salaries

| Monthly In-Hand | 50% Needs | 30% Wants | 20% Savings | Verdict |

|---|---|---|---|---|

| ₹40,000 | ₹20,000 | ₹12,000 | ₹8,000 | Hard in metros, works in Tier-2/3 |

| ₹75,000 | ₹37,500 | ₹22,500 | ₹15,000 | Workable with discipline |

| ₹1,25,000 | ₹62,500 | ₹37,500 | ₹25,000 | Comfortably works |

| ₹2,00,000 | ₹1,00,000 | ₹60,000 | ₹40,000 | Should aim for 30-30-40 instead |

| ₹3,00,000+ | ₹1,50,000 | ₹90,000 | ₹60,000 | Lifestyle-creep risk; push savings to 35–45% |

The rule is a floor for low incomes and a ceiling for high incomes — not a one-size formula.

Detailed Explanation: Where 50-30-20 Wins and Loses in India

What counts as "Needs" in India?

Needs are non-negotiable monthly outflows: rent or home-loan EMI, groceries, utilities, school fees, basic transport, insurance premiums, minimum loan EMIs, and household help. Restaurants, OTT bundles, weekend trips, and the new iPhone are wants — even if your peers call them essentials.

A common Indian mistake is dumping all EMIs into "needs". A ₹70,000 car EMI on a ₹1.2 lakh salary is not a need — it is a want that has been frozen into a 5-year contract. The rule only works if you classify honestly.

Income-bracket reality check

- ₹30K–₹50K in-hand: Rent + groceries alone can hit 55–65%. Realistic split is 65-25-10 in Tier-1 cities, 50-30-20 in Tier-2. Focus on increasing income before optimising savings.

- ₹50K–₹1L in-hand: This is the sweet spot for 50-30-20. PF already takes ~12% of basic; aim to push the 20% savings into ELSS, index SIPs and an emergency fund.

- ₹1L–₹2L in-hand: Stick to 50% needs even if you can afford more rent — lifestyle inflation is the silent killer. Push savings to 25–30%.

- ₹2L+ in-hand: Flip the rule. Target 30-30-40 (needs-wants-savings). At this income, every extra ₹10,000 saved monthly compounds to ~₹46 lakh in 15 years at 12%.

Age-wise tweaks

- 20s (single, no dependents): 40-30-30 is achievable. Maximum compounding window — every rupee saved here is worth 4–5x in your 40s.

- 30s (married, kids, EMI): Pure 50-30-20 is most realistic. Protect the 20% with an SIP auto-debit on salary day.

- 40s (peak earnings, peak expenses): Push to 50-20-30 — cut wants, accelerate retirement savings. You have ~20 working years left.

- 50s: 50-10-40. De-risk equity, top up NPS, clear all consumer loans.

Calculation Method: The Indian 50-30-20 Formula

Start from net in-hand, not CTC. Here is the formula:

Monthly In-Hand = CTC/12 − (PF + Professional Tax + Income Tax + Insurance + Other deductions)

Needs budget = In-Hand × 0.50

Wants budget = In-Hand × 0.30

Savings goal = In-Hand × 0.20

Important: EPF contribution (your 12%) already counts as part of your 20% savings. So if EPF is taking ₹3,600 on a ₹30,000 basic, your additional SIP target is (In-Hand × 0.20) − EPF.

Worked example: ₹18 LPA CTC in Bengaluru

- CTC ₹18,00,000 → in-hand approx ₹1,15,000 after new-regime tax + PF

- 50% Needs = ₹57,500 (rent ₹30K + groceries ₹12K + utilities ₹4K + transport ₹5K + insurance ₹3K + misc ₹3.5K)

- 30% Wants = ₹34,500 (eating out, OTT, gadgets, weekend trips)

- 20% Savings = ₹23,000 (EPF ₹4,800 already + SIP ₹15,000 + emergency fund ₹3,200)

If rent crosses ₹40K, the 30% wants bucket must shrink — not the 20% savings bucket. Savings is non-negotiable.

Run your actual numbers in seconds — use the FundGenie SIP Calculator to see exactly what your 20% monthly SIP will become in 10, 15 and 20 years.

Common Mistakes Indians Make With 50-30-20

- Calculating on CTC instead of in-hand — instantly inflates every bucket by 25–30%.

- Treating EMIs as savings — paying off a car loan is consumption, not wealth creation.

- Ignoring annual lumpy expenses — insurance renewals, school admission, Diwali, weddings. Park 1/12th monthly.

- Skipping the emergency fund — jumping into SIPs before having 6 months of expenses in a liquid fund.

- Confusing tax-saving with investing — ₹1.5 lakh into LIC endowment is not the same as ELSS or NPS.

- No automation — manual transfers fail. Set an auto-debit on the 2nd of every month, the day after salary credit.

- Using old tax regime by default — for many salaried Indians in 2025-26, the new regime saves more once 80C and HRA are honestly weighed.

Action Plan: Make 50-30-20 Work on Your Salary

Try On FundGenie

You don''t need a spreadsheet to know if 50-30-20 fits your salary — let our AI do the math.

- Calculate your SIP target for the 20% bucket

- Compare old vs new tax regime in 30 seconds

- Plan your retirement corpus in 2 minutes

- Check EMI affordability before any big purchase

FundGenie tip: Sign in and our AI builds a personalised 50-30-20 split using your real salary, city, EMIs and goals — not a generic template.

FAQs

Is the 50-30-20 rule realistic for Indian salaries?

Yes, for in-hand salaries between ₹50,000 and ₹1.5 lakh in most Indian cities. Below ₹40,000 in metros, rent and groceries alone push needs past 60%. Above ₹2 lakh in-hand, the rule under-saves — aim for 30-30-40 instead.

Should I calculate 50-30-20 on CTC or in-hand salary?

Always on in-hand (take-home) after PF, income tax and insurance deductions. CTC inflates every bucket by 25–30% and gives a false sense of savings capacity.

Does EPF count as part of the 20% savings?

Yes. Your 12% EPF contribution and employer match are forced retirement savings. Subtract your EPF outflow from the 20% target and invest the remainder via SIPs, ELSS or NPS.

What if my rent alone is 40% of my salary in Mumbai or Bengaluru?

Accept it short term, but cap the wants bucket at 20% and protect the full 20% savings. Plan a city or housing move within 18–24 months, or focus aggressively on income growth.

Is 50-30-20 better than the 70-20-10 rule for India?

50-30-20 is more disciplined and works better for wealth creation. 70-20-10 is closer to default Indian spending but leaves only 10% for long-term goals — insufficient for retirement given Indian inflation.

How much should I invest from my 20% savings in SIPs?

Roughly 60–70% of the 20% savings bucket can go into equity SIPs once you have a 6-month emergency fund. The rest splits across NPS, gold, and short-term debt depending on your age and goals.

Does the 50-30-20 rule include home loan EMI?

Yes — home loan EMI is a need and sits inside the 50% bucket. If the EMI alone crosses 35% of in-hand, the rule breaks and you need to either prepay aggressively or restructure.

Can I follow 50-30-20 if I am on the new tax regime in India 2025-26?

Absolutely. The rule is independent of tax regime. The new regime usually leaves more in-hand, which makes hitting the 20% savings target easier — but you lose the 80C nudge, so automate SIPs manually.

Did you find this useful?