Dual Income Couples in India: How to Manage Finances & Invest Together in 2026

A Bengaluru couple earning ₹1.8 lakh + ₹1.2 lakh per month sounds rich on paper. In reality — ₹65,000 rent, two car EMIs, a parent's medical bill, a Goa trip on credit card, and at year-end the savings show ₹40,000. Sound familiar? Dual income couples in India are the highest-earning, lowest-saving demographic, simply because no one taught us how to combine two salaries.

With inflation at 5–6%, school fees rising 10% a year, and home prices in Mumbai/Bengaluru up 18% in 2025, two Indian salaries are not automatic wealth — they need a system. This guide gives that system: how to split bills, file taxes smartly under the tax regime India offers, run joint SIPs, and protect both incomes.

Key Insights: Dual-Income Couple Money Map (₹ per month)

| Combined Income | Suggested Joint Savings | Joint SIP | Insurance (each) | Emergency Fund |

|---|---|---|---|---|

| ₹1,00,000 | ₹25,000 (25%) | ₹15,000 | ₹50L term + ₹5L health | 6 months × joint expenses |

| ₹2,00,000 | ₹60,000 (30%) | ₹35,000 | ₹1Cr term + ₹10L health | 6 months × joint expenses |

| ₹3,00,000 | ₹1,05,000 (35%) | ₹60,000 | ₹1.5Cr term + ₹15L health floater | 9 months × joint expenses |

| ₹5,00,000 | ₹2,00,000 (40%) | ₹1,20,000 | ₹2Cr term + ₹25L floater | 12 months × joint expenses |

Detailed Explanation: Managing Two Salaries the Smart Way

1. Pick a money model — don't drift

Three models work in Indian households:

- The Pool: both salaries hit a joint account, all bills paid from it, both contribute to joint SIPs.

- The Proportional Split: each pays a % of joint expenses matching their share of income (good when incomes differ a lot).

- The 3-Account System: His + Hers + Ours. Each keeps personal money; "Ours" runs household + investments. Most popular in urban India 2026.

2. Split bills before lifestyle inflation eats both salaries

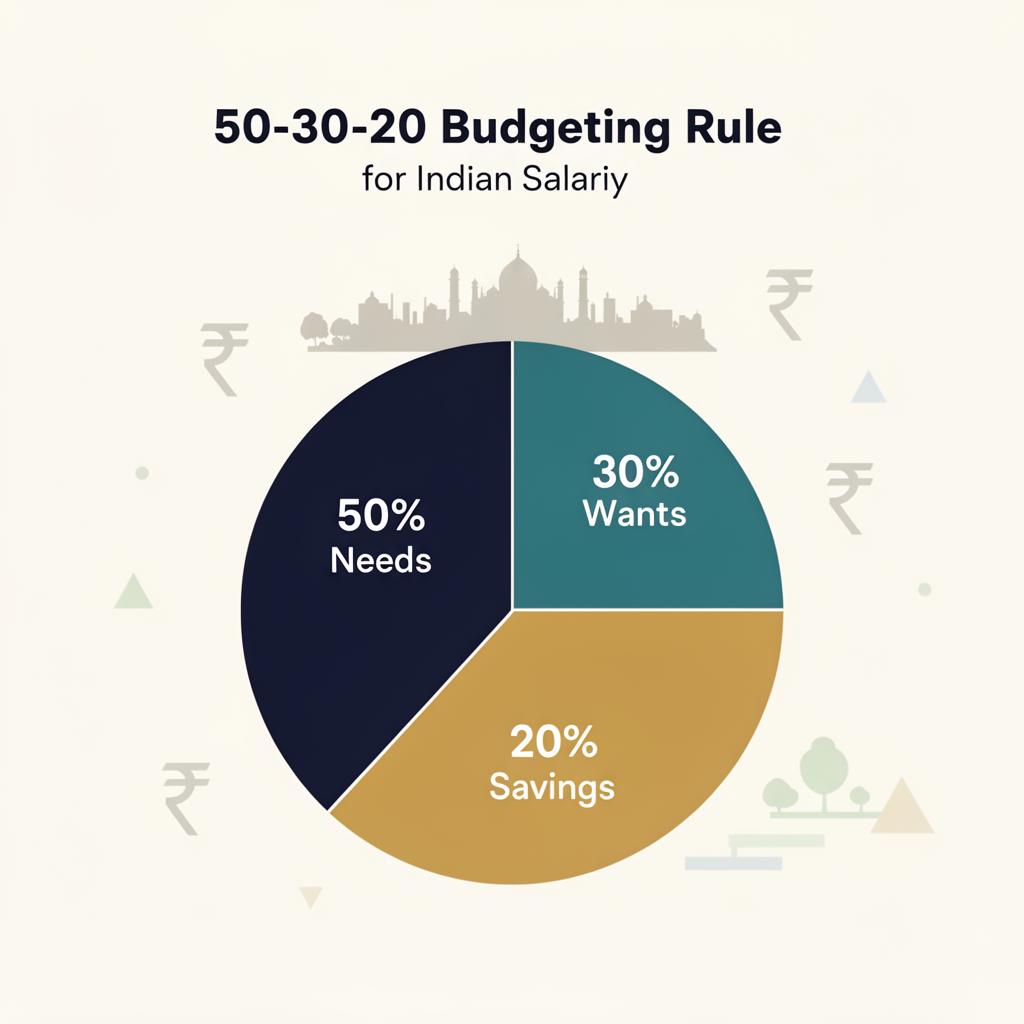

Use the 50-30-20 rule on combined income, not individual:

- 50% needs (rent, EMIs, groceries, utilities, kids)

- 30% wants (eating out, travel, gadgets)

- 20% minimum savings + investments

3. Tax-optimise as a couple, not as individuals

Under the tax regime India 2026 offers:

- Put the home loan in joint names — both claim ₹2 lakh interest (Sec 24) + ₹1.5 lakh principal (80C) = ₹7 lakh combined deduction.

- Put rent paid in the higher-earner's name for full HRA exemption (old regime).

- Run health insurance for parents in the lower-bracket spouse's name (saves nothing if both in 30% — split equally).

- Open PPF in both names = ₹3 lakh tax-free saving per year.

4. Two NPS accounts = ₹1 lakh extra deduction

Each spouse can claim ₹50,000 under 80CCD(1B) — combined ₹1 lakh extra over the ₹1.5L 80C limit. Old regime only.

Age-wise Joint Money Priorities

| Stage | Priority 1 | Priority 2 | Priority 3 |

|---|---|---|---|

| 25–30 (newly married) | Emergency fund + term insurance | Joint SIP ₹15–25K | Skill upgrade |

| 30–35 (first child) | Health floater + child SIP | Home loan / down payment | Increase term cover |

| 35–45 (peak earning) | Retirement SIP ₹40K+ | Child education goal | Real estate / second income |

| 45–55 (pre-retirement) | NPS Tier-1 max | Debt-free home | Healthcare corpus |

Mid-article CTA: Project what your joint ₹35,000 SIP becomes in 15 years with annual step-up. Use the FundGenie SIP Calculator — built for Indian markets and tax.

Calculation Method: The Couple's Financial Health Formula

1. Joint Savings Rate

(Combined income − Combined expenses) ÷ Combined income × 100

Healthy = 25%+. Below 15% = lifestyle inflation. Above 40% = on track for early retirement.

2. Joint Debt-to-Income

Total EMIs ÷ Combined take-home

Keep under 40% (RBI safe lending limit). Above 50% = stress zone.

3. Combined Term Cover Needed

(Annual joint expenses × 15) + outstanding loans − liquid assets

Split based on income share. A couple spending ₹15L/year with a ₹50L home loan needs ~₹2.75 Cr combined cover.

4. Joint SIP Future Value

FV = P × [((1+r)^n − 1) ÷ r] × (1+r)

At ₹35,000/month, 12% return, 15 years, 10% step-up → ~₹2.4 Cr corpus.

Common Mistakes Indian Couples Make

- No joint financial review. Money is the #2 reason for divorce in urban India — silence is the cause.

- Both buying the same ELSS/LIC. Duplicate 80C, zero diversification.

- Lifestyle inflation after marriage. Two incomes → two cars → two EMIs → zero savings.

- No term insurance for the non-earning or lower-earning spouse. Their financial value (household, childcare) is real.

- Joint locker but no joint will/nomination. Nominee disputes block accounts for months.

- Single bank account in one name. Operationally fragile if one spouse is unwell or travelling.

- Investing only in one spouse's name to "save tax" — capital gains and wealth concentration become problems later.

Action Plan: 30-Day Money Setup for Dual-Income Couples

Week 1 — Visibility

- List all incomes, EMIs, SIPs, insurance policies on one sheet.

- Open a joint savings account (any major Indian bank — instant via net banking).

Week 2 — Protection

- Buy/upgrade term cover for both (15× annual income each).

- Buy a family floater health insurance (₹10–25 lakh sum insured).

- Add nominees to every bank, mutual fund, EPF, NPS.

Week 3 — Tax & Investment

- Decide regime per spouse using the FundGenie Tax Calculator.

- Start a joint SIP — minimum 20% of combined income, increase 10% yearly.

- Open NPS Tier-1 for both (₹50K each).

Week 4 — Goals

- Define 3 joint goals: emergency fund, home down payment, retirement.

- Assign a separate SIP to each goal — never mix.

- Schedule a monthly 30-minute money date. This single habit beats every app.

Try on FundGenie

Doing all this on Excel is why 70% of Indian couples never reach their goals. Let the calculators do the math:

- SIP Calculator — joint SIP with step-up, goal-mapped projections.

- Tax Calculator — compare regimes for both spouses in 30 seconds.

- EMI Calculator — joint home loan, joint deduction, joint affordability.

Plan your retirement in 2 minutes — start the FundGenie SIP Calculator.

FAQs

How should dual income couples in India split their bills?

The most flexible system is the 3-account model: each spouse keeps a personal account, and a joint account funds rent, EMIs, groceries, utilities, and SIPs. Contribution can be 50:50 or proportional to income — proportional is fairer when one spouse earns significantly more.

Should husband and wife file taxes separately in India?

Yes — India does not allow joint filing. Each spouse files individually. The tax optimisation happens by splitting investments, home loan, and rent intelligently across both PANs to maximise deductions under both old and new regimes.

Can both spouses claim home loan deduction in India?

Yes, if the property and the loan are in joint names and both are co-borrowers contributing to EMI. Each can claim up to ₹2 lakh interest (Sec 24) and ₹1.5 lakh principal (80C) — a combined deduction of up to ₹7 lakh per year under the old regime.

How much should a dual income couple save every month in India?

Aim for 25–40% of combined take-home — higher if you're DINK (double income, no kids) in your 20s/30s. A couple earning ₹2 lakh combined should target ₹50,000–₹70,000/month into emergency fund, SIPs, and retirement.

What insurance should married couples in India buy?

Two separate term plans (15× annual income each), one family floater health insurance of ₹10–25 lakh, and a separate health cover for dependent parents. Avoid duplicate endowment or ULIP policies — they kill returns.

Is it better to have joint or separate bank accounts after marriage?

Best practice in 2026 is one joint account for shared expenses plus individual accounts for personal money. Pure pooling causes friction; pure separation makes goals slow. The 3-account hybrid is what most urban Indian couples settle on.

How can a couple save tax on rent in India?

If only one spouse receives HRA and you live in rented accommodation, pay rent from that spouse's account and claim full HRA exemption. If both receive HRA, split rent receipts proportionally. Both can claim — but only against actual paid amounts with valid PAN of landlord (rent above ₹1 lakh/year).

How much corpus does a dual income couple need to retire in India?

Rule of thumb: 25× your annual expenses at retirement, inflation-adjusted. A couple spending ₹10 lakh today, retiring in 25 years at 6% inflation, will need ₹43 lakh/year — meaning a corpus of about ₹10.7 crore. Start a joint SIP of ₹40,000+ today to get there.

Did you find this useful?