If you bring home around ₹50,000 per month in India in 2026, you are not poor — but you are not free either. Rent in Tier-1 cities crosses ₹15,000, grocery inflation is running at 6-7%, and a single hospital visit can wipe out months of savings. The truth is, most ₹50K earners feel "stuck" not because of income, but because of how money is split. With the right budget, tax regime choice, and a small SIP, the same salary can build a ₹1 crore corpus in 20 years. This guide gives you the exact numbers — budget split, tax math, SIP plan, EMI limits, and the mistakes to avoid.

Quick Snapshot: ₹50,000 Salary Plan (India 2026)

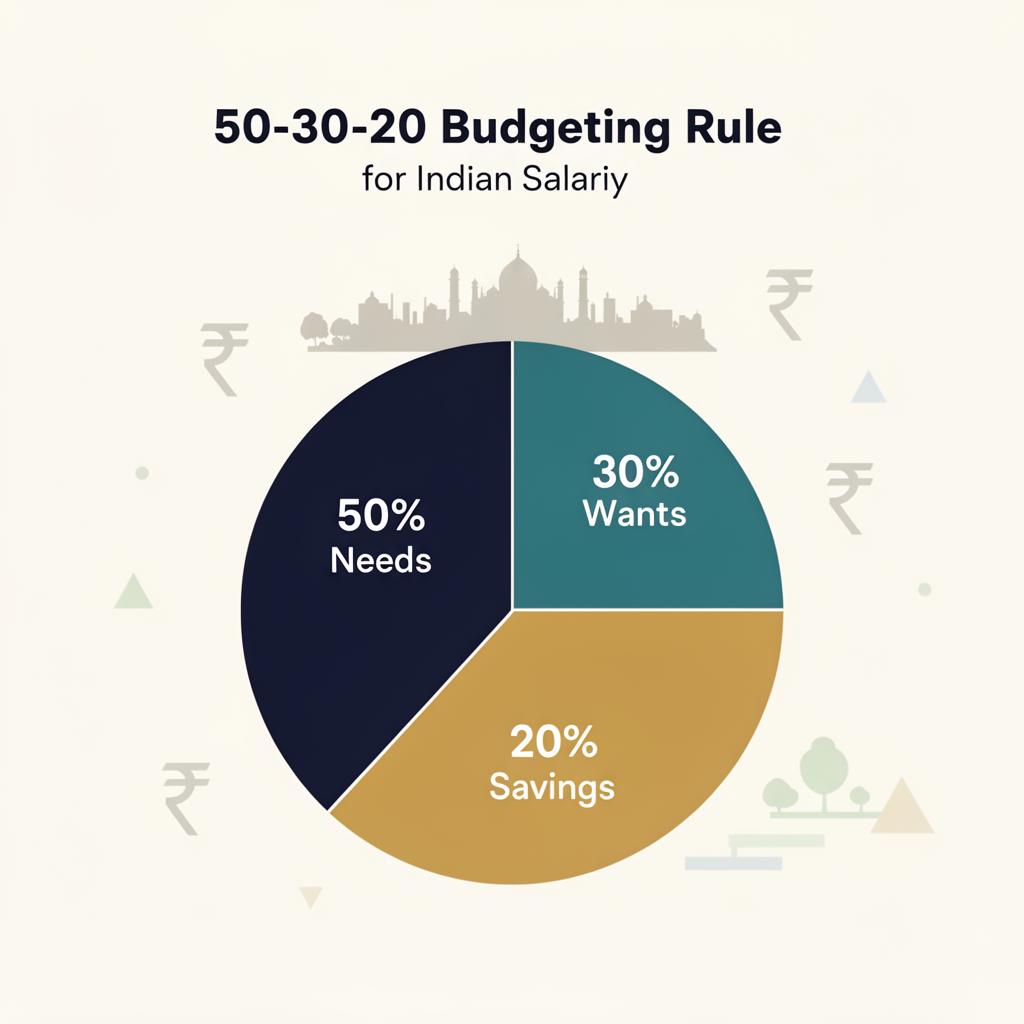

| Bucket | Monthly | % of Salary |

|---|---|---|

| Needs (rent, food, bills, transport) | ₹25,000 | 50% |

| Wants (eating out, OTT, shopping) | ₹10,000 | 20% |

| SIP + Emergency Fund | ₹10,000 | 20% |

| Insurance + Tax-saver | ₹5,000 | 10% |

Tax under new regime (FY 2026-27): ₹0 (income below ₹12 L rebate slab after standard deduction). SIP at 12% CAGR for 20 years: ₹10,000/month → ~₹99.9 lakh corpus.

Detailed Breakdown by City Type

Tier-1 (Mumbai, Bengaluru, Delhi NCR)

Rent eats 35-40% of salary. A shared 1BHK at ₹18,000 + ₹4,000 utilities leaves only ₹28,000 for everything else. SIP must drop to ₹6,000-7,000/month, and you should aggressively negotiate WFH or shift to a cheaper micro-market (Thane, Whitefield, Noida Extension).

Tier-2 (Pune, Hyderabad, Ahmedabad, Jaipur)

Rent of ₹10,000-12,000 frees up ₹6,000-8,000 extra. This is the sweet spot — a ₹50K salary in a Tier-2 city has the same lifestyle as ₹75K in Mumbai. Push SIP to ₹12,000/month.

Tier-3 / Hometown

Living with family? Bank 50-60% of salary. A ₹25,000/month SIP for 15 years at 12% builds ₹1.26 crore. This is the fastest wealth path on a ₹50K salary.

Age-wise Allocation

- 22-27 years: 70% equity SIP (index + flexi-cap), 20% liquid fund, 10% term + health insurance.

- 28-35 years: 60% equity, 20% PPF/EPF, 10% gold ETF, 10% emergency fund.

- 35+ on ₹50K: Prioritise debt reduction and skill upgrade; salary growth matters more than asset allocation.

Tax Calculation: New vs Old Regime on ₹6 Lakh CTC

Gross annual = ₹6,00,000. Standard deduction = ₹75,000. Taxable = ₹5,25,000.

- New regime (default 2026): Tax = ₹0 (rebate u/s 87A applies up to ₹12 L taxable).

- Old regime: Even with ₹1.5 L 80C + ₹25K 80D, tax = ₹0 after 87A rebate.

Verdict: New regime wins for ₹50K salary because you don''t need deduction proofs and take-home is higher month-on-month. Switch only if your home loan interest crosses ₹2 L/year.

Check your exact liability on the FundGenie Tax Calculator — it compares both regimes side by side in 30 seconds.

SIP Math: How ₹10,000/month Becomes ₹1 Crore

Future Value of SIP = P × [((1+r)^n – 1) / r] × (1+r), where r = 12%/12 = 0.01, n = 240 months.

- ₹10,000 × 240 months × 12% CAGR = ₹99.9 lakh

- Step-up SIP (10% annual increase): same plan → ₹1.95 crore

A simple 10% step-up every April (when your appraisal hits) nearly doubles your corpus without feeling the pinch.

EMI Rule: What You Can Safely Borrow

Total EMI should never cross 40% of take-home on a ₹50K salary. That''s ₹20,000/month max — and that includes car loan, credit card, and personal loan combined. For a home loan at 8.5% over 20 years, ₹20,000 EMI supports a loan of only ~₹23 lakh. Don''t let a builder or banker push you past this.

7 Common Mistakes ₹50K Earners Make

- Buying a ₹10 lakh car on EMI before building emergency fund.

- Picking ULIPs sold by relatives instead of term insurance + mutual fund.

- Skipping health insurance because "company covers it" — it ends the day you resign.

- Investing in 8-10 mutual funds (3 is enough: large-cap index, flexi-cap, ELSS).

- Using credit card EMI for lifestyle purchases (effective rate 24-36% p.a.).

- Choosing old tax regime out of habit when new regime gives zero tax.

- Treating bonus/Diwali money as "extra" instead of pushing into SIP top-up.

Action Plan: First 90 Days

Try on FundGenie

✅ Plan your SIP for ₹50K salary on FundGenie → Get a personalized monthly investment plan in 2 minutes.

FAQs

Is ₹50,000 a good salary in India in 2026? It is decent in Tier-2/Tier-3 cities and tight in Mumbai/Bengaluru/Delhi. A disciplined ₹50K earner in a Tier-2 city can save 30-40% of income; the same salary in a metro typically saves 10-15%.

How much tax do I pay on ₹50,000 monthly salary? Zero under the new tax regime for FY 2026-27, because taxable income (₹5.25 L after standard deduction) is below the ₹12 L rebate threshold u/s 87A.

How much SIP should I do on ₹50,000 salary? Aim for ₹8,000-12,000/month (16-24% of salary). Even ₹10,000/month at 12% CAGR builds ~₹1 crore in 20 years.

Should I choose old or new tax regime on ₹50,000 salary? New regime is better for almost all ₹50K earners — higher take-home, zero tax, no proof submission. Switch to old only if home loan interest exceeds ₹2 L/year.

Can I buy a house on ₹50,000 salary in India? Yes, but cap the EMI at ₹20,000/month. That supports a ~₹23 L home loan at 8.5% for 20 years. Buy in Tier-2 cities or peripheral metro areas.

How much emergency fund do I need on ₹50K salary? Minimum 6 months of expenses — typically ₹1.5 to ₹2 lakh — in a liquid fund or sweep-in FD.

Is ₹10,000 SIP enough to retire? ₹10,000/month for 30 years at 12% CAGR builds ~₹3.5 crore. With a 10% annual step-up, it crosses ₹9 crore — enough for a comfortable retirement.

What insurance should a ₹50K earner have? ₹1 crore pure-term life insurance (~₹700-900/month at age 28) and ₹5-10 lakh family floater health policy. Avoid ULIPs and endowment plans.

Related reads: 50-30-20 Rule for Indian Salaries · NPS vs ELSS Tax Saving · ₹1 Lakh Salary Plan

Did you find this useful?